Background to Insurance Linked Securities (ILS)

Since the 1990’s there has been a strong growth in the ILS market. Insurance and re-insurance firms looking to offset their risk have increasingly leveraged the financial markets via the securitization of their assets and liabilities.

The ability to package and securitize policies has enabled the insurance firms to pass on their exposure to financial investors, reducing their risk of losses in a capital efficient way (i.e. reduced risk results in a reduction in the level of capital required for existing business thereby enabling them to write more new business with the same level of capital)

The capital providers like these types of securities as they:

- Provide non-correlated returns (i.e. not tied to the economic cycles/performance of the markets but driven by insurance loss events) and therefore provides diversification for investment portfolios.

- Generate high returns (i.e. coupons) compared to equivalent rated fixed-income products (e.g. Schroder GAIA fund investing predominantly in Cat Bonds had average yield of 9.5% @ 30th August 2019).

- Are generally low-volatility, tradeable, liquid notes.

In 2018 the ILS market reached $93Bn, up from $88Bn in 20171, with a CAGR between 2009 and 2018 of 20%. One segment of the insurance linked securities market is the reinsurance of high severity, low probability events known as CAT bonds, or catastrophe bonds (e.g. cover for natural disasters and other uncontrollable events).

The insurance firms are using investment banks to sell these securities to investment firms, also known as “capital providers”. These investment firms are often asset managers or hedge funds looking to generate alpha2 , especially in the current low-interest markets where returns are challenged.

Cat bonds are generally short-term (3-5-year duration), high risk fixed income products (~BB rating), often issued as floating rate bonds (i.e. coupon linked to an underlying benchmark such as LIBOR with spreads between 3 & 20%). The value ideally would be the expected loss from the occurrence of an insurance event underwritten by the policies packaged in the security.

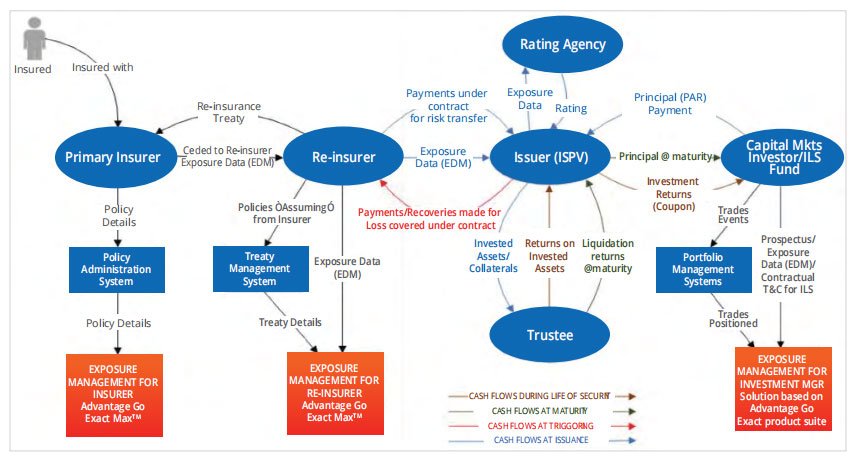

As stated, an ILS transaction involves an insurance or reinsurance firm (known as a “cedant”) transferring specific exposures to a special purpose vehicle3 . The terms of this transaction are governed by contracts for risk transfer. The ISPV then issues securities to investors to raise capital to cover the insurance exposure.

The capital provider invests the principal in return for a coupon funded by the premiums paid to the insurance/ re-insurance firm (i.e. the issuer or guarantor).

In the event of a catastrophe that triggers the contract for risk transfer (i.e. payment to cover loss) then the capital provider loses part, or all the principal invested as this is used by the insurance firm to cover the resulting losses.

ILS transactions typically include a facility to safe keep the principal raised to ensure adequate collateral to meet the obligations defined under the contract (i.e. to the cedant and the investors).

Other common types of ILS include securitized insurance derivative contracts such as Collateralised reinsurance transactions4 , CAT Swaps, Embedded Value Securitization5, Extreme Mortality Securitization6, Life Settlements Securitization and Longevity Swaps7.

For glossary of terms see

Advantage Go Products for Exposure Management within the Insurance Market

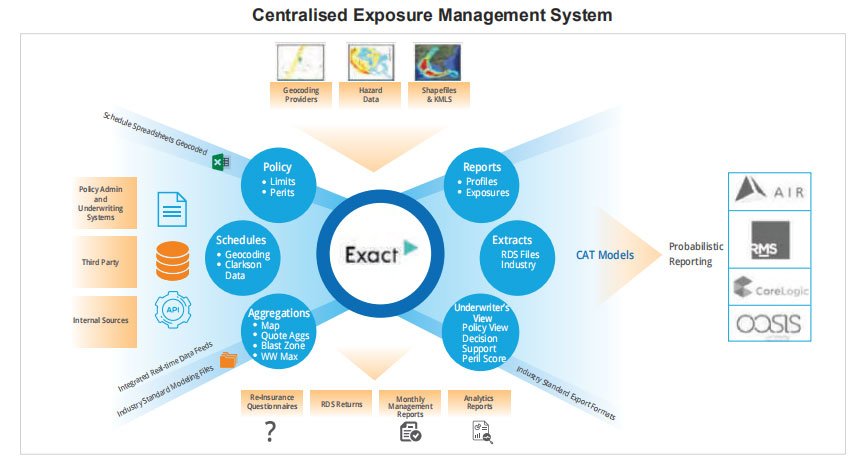

Exact™ is an exposure management solution targeted at the Insurance underwriters, providing the ability to manage accumulations of risk across all lines of business for all regions and businesses.

Exact Max™ provides a similar (albeit extended) type of functionality but focused on the Global Re-insurance market, the key difference between the solutions is the volume of data supported, with Exact Max™ being able to process and visualize huge volumes of data in realtime (i.e. billions).

They are proven, extremely effective data aggregation engines with market leading analytics capabilities.

The solutions incorporate integrated hazard scoring with built in dashboards and ad-hoc reporting capability. Features include:

- Import of scheduled and real-time data from policy administration and underwriting systems, third party systems and other sources using industry standards (e.g. EDM modelling files).

- Importing, validating and augmentation of data using Geocoding, Hazard Scoring and Geospatial services.

- Provide catastrophe data feeds to probabilistic reporting solutions used for risk modelling (e.g. RMS, AIR, CoreLogic, Oasis).

- Identify accumulations including hidden accumulations from a portfolio

- Identify accumulations from a portfolio and then visualize using the integrated Google maps view to provide risk assessment of events such as terrorism, fire and earthquakes.

- Calculation and tracking of potential losses in realtime for catastrophic events.

- Ability to validate that new business is within defined risk appetite thresholds.

- Monitoring of exposures at company and group levels with ability to set limits, suspend activity etc. with full integration with Dun & Bradstreet data.

Our View

We believe that there is an opportunity to leverage the Advantage Go Exact™ and Exact Max™ product set to provide a compelling solution for the Capital Providers.

Loading of positions, orders and executions and overlaying the policies, the geocoding, the hazard scores etc. would enable firms to have a far better view on their market risk, also to enable effective pre-trade validation and pre-emptive warnings on events that could impact returns.

Capital Providers would also be able to leverage the functionality to identify key areas of the world where risk from multiple investments correlates together, thus changing their worse-case exposure to risk. As more and more business is transacted in this way, the leaders will be those companies who are best placed to understand their underlying risks in detail, and make informed decisions on that basis.”

Let us discuss.

- Based on report from Willis Re published in

- Alpha is a measure of the active return on an investment, the performance of that investment compared with a suitable market index. An alpha of 1% means the investment’s return on investment over a selected period of time was 1% better than the market during that same period; a negative alpha means the investment underperformed the market.

- Known as Insurance Special Purpose Vehicle or ISPV.

- Similar to conventional reinsurance arrangements such as CAT bonds but deals tend to be smaller in scale, also, whereas CAT bonds are used to raise capital by public offerings, these are privately placed with smaller group of specialized investors or ILS investment funds.

- Calculated by adding the present value of future profits of a firm to the net asset value of capital and surplus. When securitized in the form of an asset backed note, the principal repayment is linked to the emergence of future profits (i.e. enables an insurance firm to monetize the captured value of a block of business).

- Like CAT bond, where an event results in a high level of mortality.

- Transfers the risk of pension scheme members living longer than expected from pension schemes to an insurer/bank provider.